Correction to Tree Grower Article

Meeting future challenges with Innovation

NZ Tree Grower August 2025

Graham West

Throughout history we have used the saying “Necessity is the mother of invention.” Right now, I think we are staring down the barrel of necessity. We are facing an unprecedented need for rapid change through innovation in forest growing. This may require considerable investment, and it will require a change in thinking.

Executive summary

Recently there has arisen serious questions over the future profitability of forest growing in New Zealand, and to address these we all need to be aware of the possible future ahead. The main challenges are:

- A six-year trend of increasing costs of production, coinciding with a reduction in log prices, that leading to zero or negative stumpages or profit.

- An expected reduction in demand for log from China over the next 5 – 10 years creating a long period of over-supply of logs for the local market.

- Slow progress in diversification of species, products and markets of higher value to offset rising costs.

- Extremes of climate impacting the resilience of forests, particularly affecting forest health and yield, and

- A lack of social license and government support to create a more resilient and sustainable forestry sector.

Most large-scale growers recognise the problems but have not yet chosen to invest in the risky forest innovation projects needed to find the step change that will make a difference. Some have made considerable investment in species trials and building strategic awareness.

Small scale growers are less aware and have some flexibility to mitigate these challenges by delaying harvest or switching to permanent carbon regimes. However, the above challenges pose a threat to those small growers relying on a cash contribution during pastoral downturns, or to fund their retirement or farm succession transaction .

What can the NZFFA do? First, make sure all small-scale growers are aware of these future challenges and ask if they think the present levels of innovation investment are sufficient. Second, encourage small-scale growers to act more collaboratively. By forming stronger representative associations, they can help prepare for and mitigate future risks.

Introduction

The core problem for the sector is that commercially, we are going backwards. If we review the last 20 years it’s clear that despite the Levy system and government science programmes, we have not generated innovation fast enough to keep pace with rising production costs and market competition. Some of the reasons for this are:

- Health and safety concerns have driven greater capital investment in harvesting mechanisation; capital costs have increased supply chain costs.

- Societal concerns about water quality and off-site impacts have increased compliance costs.

- Despite significant research programmes, forest productivity has not significantly increased since the early gains from tree breeding and operational best practice.

- Levy investments in research are primarily driven by annual projects or fixed 6-year consortia programmes. To date these investments have not been focussed on the emerging challenges.

- The scale of levy funding has not met the scale of the strategic problems.

The Forest Growers Levy Trust Board strategy meeting in October 2024 produced five significant priorities that needed to be addressed. One of these was:

Advancing industry resilience, including initiatives to improve preparedness to adapt to adverse climate, market and other changes.

Following that, there was a levy funded Resilient Forest Design workshop in March this year that produced a greater awareness of the broad range of challenging issues confronting the sector, including margin compression and markets. It made progress with analysing the drivers of change, and in agreeing that greater pan sector collaboration was needed.

The Levy priority above has not yet significantly changed the research programme to address these challenges. However, some good results that should help resilience issues in the short term are being achieved by modellers and spatial analysts at Scion (e.g. Watt et al., 2024 and 2025).

The biggest challenges

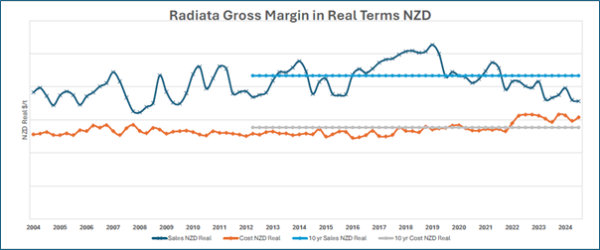

What most forest growers recognise is the trend in erosion of gross margins or net profit. This has particularly occurred over the last five years, and it is likely to get worse if the Chinese market reduces consumption, as the Japanese and Korean export log markets did in previous eras. Figure 1 gives an analysis of recent costs and returns provided by Ian Hinton (Timberlands) in his presentation to the Resilient Forests Design workshop in March. It shows in real terms in $/tonne, the last 20 years of radiata pine sales revenue (blue) and costs (orange). For fifteen years margins were maintained, but in the last five years the margin squeeze has become obvious. When these lines cross, real net profit becomes zero or negative. However, for those using a 10 year average the trend appears flat.

Figure 1; Radiata pine gross margin in real terms - NZD - Ian Hinton, Timberlands, 13 March 2025

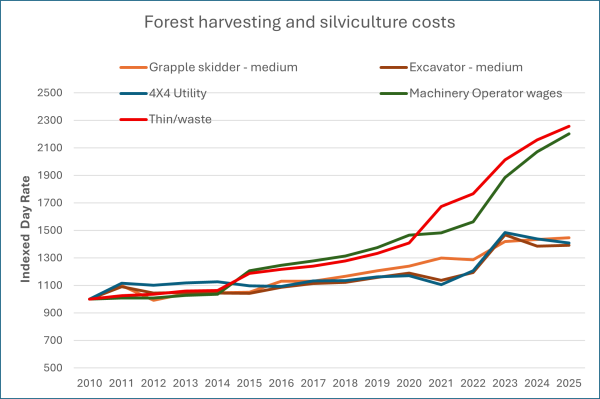

An analysis of harvest net returns since 1989 by John Schrider (2025) shows a similar trend. Since 2018 he has identified a rapid decline in stumpage across all five harvesting options in the study. It is most pronounced for an unpruned woodlot with high harvest and transport costs. From a costing database provided by Forme Consulting Group, harvesting and silviculture cost trends can be analysed (index from 1000 at 2010). What is notable from the results (given in figure 2) is the rapid increase in costs over the last five years, particularly when associated with wages.

Figure 2: Forest harvesting and silviculture costs

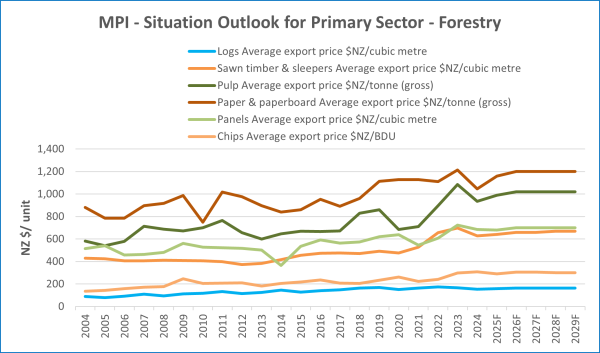

Despite MPI forecasting that the forestry sector will maintain current levels of export earnings for the next four years (Situation and Outlook for the Primary Sector, 2025) there is little mention of the effect of rising costs. Also, if we consider the trend shown in Figure 3 of wood product prices not adjusted for inflation, there has been little change over 20 years, particularly for export logs. We know that the Chinese market absorbs about 60% or 20 m tonnes/yr of our radiata logs, and the lack of alternative markets for this huge volume of wood presents a major threat to our future domestic log prices.

Figure 3: Average export prices for forestry by product, not adjusted for inflation.

While the emerging Indian log trade may offer an alternative, the forest growing sector cannot continue with the high-risk business model of sending 60% of its logs to one market.

Increasing risks from climate change have been well explored in workshops and science papers in previous decades (Dunningham et al. 2012). Damage from wind, high intensity rain, and forest health incursions can be economically significant. However, the loss of markets could be equally catastrophic, yet innovation into new species and alternative products to raise product value is getting little support.

Sector improvement through rationalisation and scale

Most primary sectors face rising production costs and attempt to mitigate these by applying innovation to lift the value of their end products or reduce the costs of delivery. This can be through working smarter or using economies of scale. Pastoral farming has adopted these strategies; farms have amalgamated and even corporatised in attempts to reduce overheads and stay profitable. Between 2002 and 2019 the total number of farms in New Zealand dropped from 69,510 to 49,530 – a 28.7% decrease (Stats NZ).

Investors in the sawmilling sector have likewise undergone decades of attrition through market competition. Around 30-40 sawmills have closed in the last 10 years allowing the successful mills to scale up and maintain margins.

Up until recently, all forest growers have been supported by a volatile but reasonably priced and absorbent Chinese log market. This has allowed both large growers and small growers to make acceptable returns (Evison, 2025; West, 2019) for at least the last 15 years. Some amalgamation of medium sized forests has occurred in the last six years, this has increased the area of forests now in the >10,000ha NEFD category and reduced area in the 1000 – 9,999 ha category. (MPI 2024 - National Exotic Forest Description, NEFD). Data on small forest growers is limited but this group don’t appear to be amalgamating forest ownership and generally seem unwilling to cooperate in marketing or supply as we have seen with dairy farmers. Perhaps this is because each small forest is an investment, not a business. Owners wish to maintain the flexibility to cash in a woodlot when it suits their personal circumstances. However, the challenges emerging place these owners at greatest risk.

Moving forward

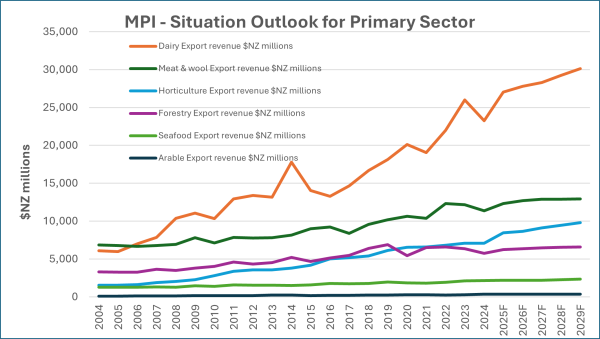

Other primary sectors with similar challenges could be analysed for solutions. Most have been more successful than Forestry, as shown in figure 4 (MPI, 2025). The dairy and horticulture sectors stand out. The dairy industry formed the Fonterra Cooperative in 2001 and has been a major success for New Zealand. Dairy export earnings (orange) that were $6 bn a year in 2004 had grown to $27 bn by 2025. Over the same period forestry export earnings (purple) went from $3.5 bn a year to just $6 bn. Both industries use about the same land area although to be fair, forestry sold some of its good land to dairy farmers to release capital and moved on to hill country where the returns have been lower.

The structure and marketing methods of the forest growing sector could be re-examined for innovative ways to capture the sort of benefits the Dairy sector and Kiwifruit industry have achieved. NZFFA has invested in several studies to illuminate and solve this problem, (Levack and Moore, 2010).

What might be needed is to facilitate high risk innovation projects through a separate innovation entity. Several of these exist in the primary sector, for example, Agmardt (Agricultural and Marketing Research and Development Trust), Seafood Innovations Ltd, Wool Industry Research Ltd (WIRL), DairyNZ – On-Farm Innovation Fund. The key is the entity is driven by urgency and has a focus on commercial innovation with some autonomy to act via a separate board with its own criteria for evaluating project proposals.

I believe the NZFFA should promote a similar model. It would seek requests for proposals with strict guidelines and be open to all interested parties. It’s important specify a need for step change ideas and encourage critical thinkers and risk takers. Funding for this model could come from the NZFFA reserves and / or the Primary Sector Growth Fund.

Figure 4: Export earnings by primary sector in NZ 2004 – 2024 and forecast

Examples of the major challenges this innovation group would take on are:

- How to make a substantial reduction in supply chain costs

- What innovations would lead to a substantial increase in the value of wood products.

- Provide a conduit and engage the best minds in New Zealand across multiple disciplines to help the forest industry find the future opportunities.

If this sounds like the Forestry and Wood Processing Industry Transformation Plan from 2022, it not surprising, the challenges haven’t changed much in three years, and the current research approach is not creating change fast enough.

More grower collaboration would help. Partnerships may spin off and the new government Primary Sector Growth Fund may find this attractive. The fund’s stated objective is to “focus on practical projects that reduce costs across the food and fibre sector value chain and deliver stronger returns on investment to the farm and forest gate.”

Major targets for investment need to come from the forest owners with appropriate rationale. We could aim for 50% of the research programme committed to higher risk and longer-term projects, recognising that these will need intense monitoring to achieve the desired outcomes.

Conclusion

We all hope the negative trends given here don’t occur. Regardless, small-scale growers should be informed and engaged in the future challenges they may face. Debate is needed on whether business as usual in terms of research spend and our view of innovation risk will achieve the desired rate of change. In my view, major changes are needed, and this will not come from incremental research. It is acknowledged that step change innovation is high risk but, perhaps not as risky as business as usual. Understanding and managing risks is important, but building sector resilience is going to require innovation.

To help prepare for and mitigate the future, small-scale growers should be encouraged to act more collaboratively, forming stronger representative associations, sharing costs, and acting pan sector. The NZFFA has a role in this but so too has NZ Forest Owners Association, Te Uru Rakau/NZ Forest Service, Nga Pou a Tane, and various farming organisations. If the government wants to double exports in 10 years, it has a role in funding risky innovation projects that leads to that level of revenue step change.

References

Dunningham, A., Kirschbaum, Payn, T., Meason, D. 2012. Chapter 7, Long term adaption of productive forests in a changing climatic environment. In, Impacts of Climate Change on land-based sectors and adaption options. Stakeholder report. Ministry of Primary Industries. SLMACC.

Evison, D. 2025. Investment returns from New Zealand’s large-scale commercial forests 2009 to 2023. NZ Journal of Forestry, February 2025, Vol. 69, No. 4

Levack, H., Moore, H. 2010. What is the NZFFA role in facilitating well designed forestry cooperatives? NZ Tree Grower, May 2010

Ministry of Primary Industries. 2024. National Exotic Forest Description. 66273-National-Exotic-Forest-Description-2024-report.pdf

Ministry of Primary Industries. 2025. Situation and outlook for primary industries (SOPI). https://www.mpi.govt.nz/dmsdocument/69612-Situation-and-Outlook-for-Primary-Industries-SOPI-June-2025

Schrider, J. 2025. A rethink on how we harvest our small forests. New Zealand Tree Grower, May 0225.

Watt, M.S.; Holdaway, A.;Watt, P.; Pearse, G.D.; Palmer, M.E.;Steer, B.S.C.; Camarretta, N.; McLay, E.; Fraser, S.2024. Early Prediction of Regional Red Needle Cast Outbreaks Using Climatic Data Trends and Satellite-Derived Observations. Remote Sens. 2024, 16, 1401. https:// doi.org/10.3390/rs16081401

Watt, M.S.; Holdaway, A; Camarretta, N.; Locatelli, T; Jayathunga, S.;Watt, P.; Tao, K.; Suarez,J.C. 2025. Mapping Windthrow Risk in Pinus radiata Plantations Using Multi-Temporal LiDAR and Machine Learning: A Case Study of Cyclone Gabrielle, New Zealand. Remote Sens.2025, 17, 1777. https://doi.org/10.3390/rs17101777

West, G.G. 2019. Results of survey for small-scale forest harvesting. NZ Tree Grower, Aug 2019